.NET Suite for your Trading Applications

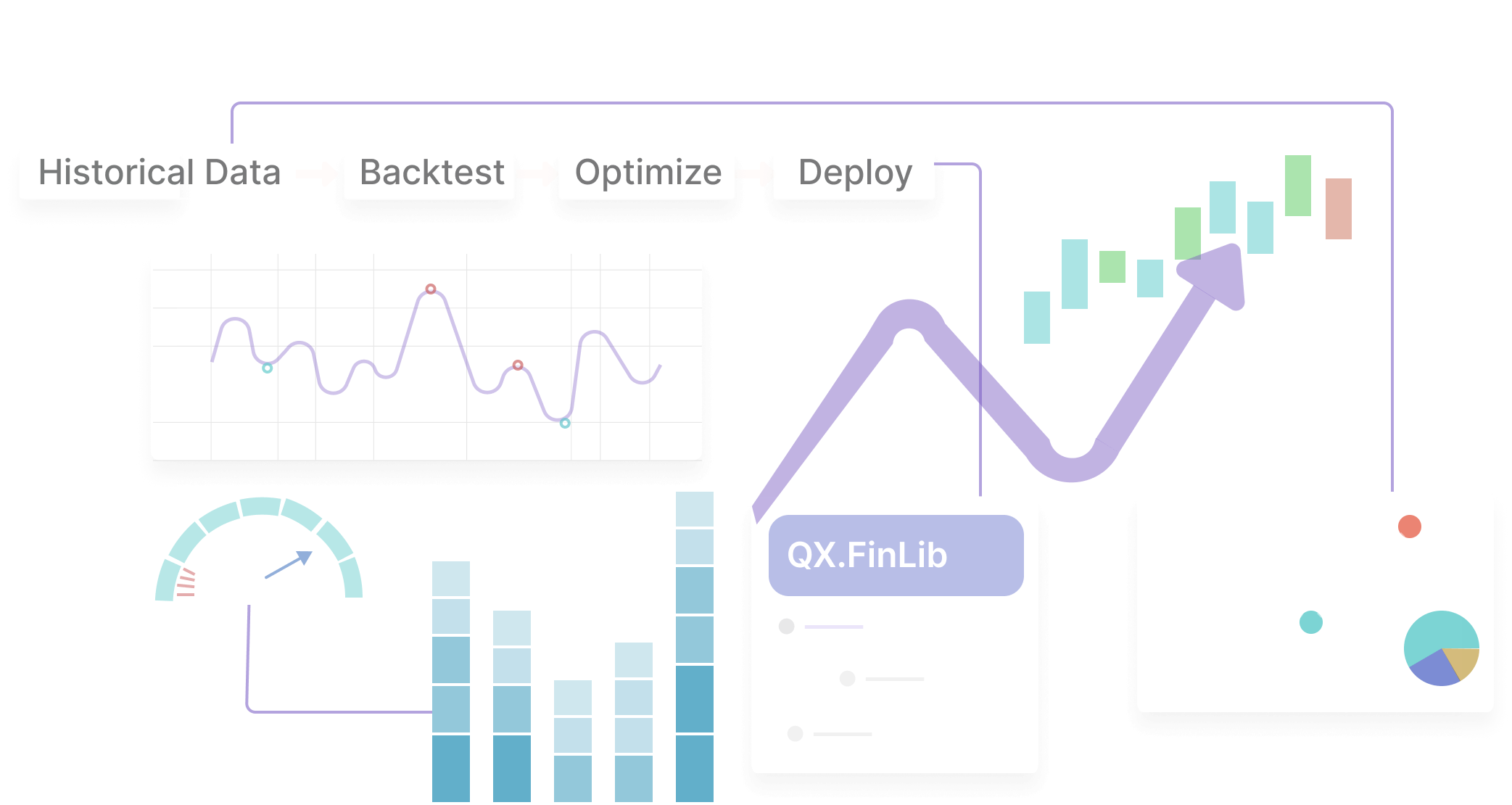

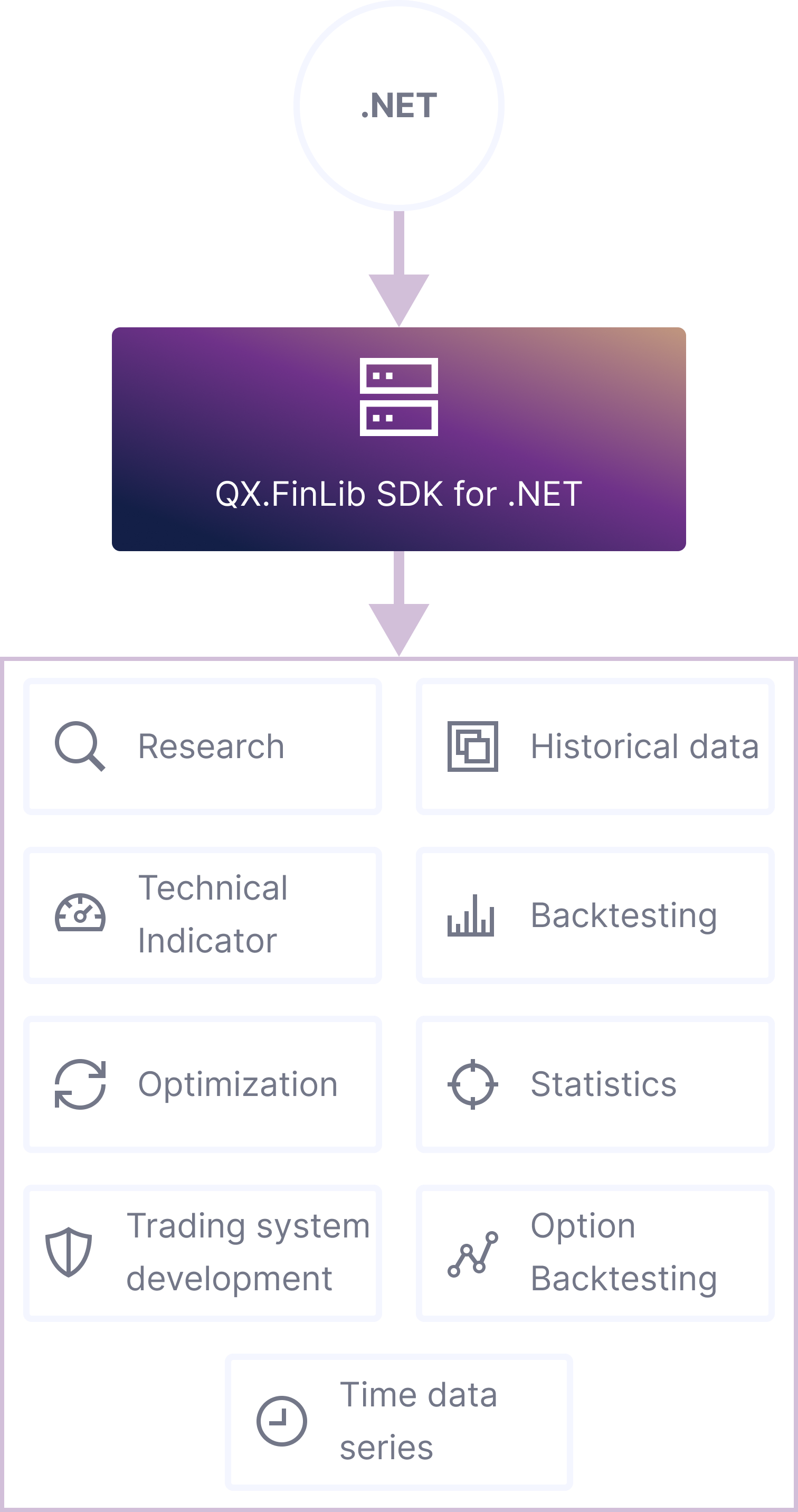

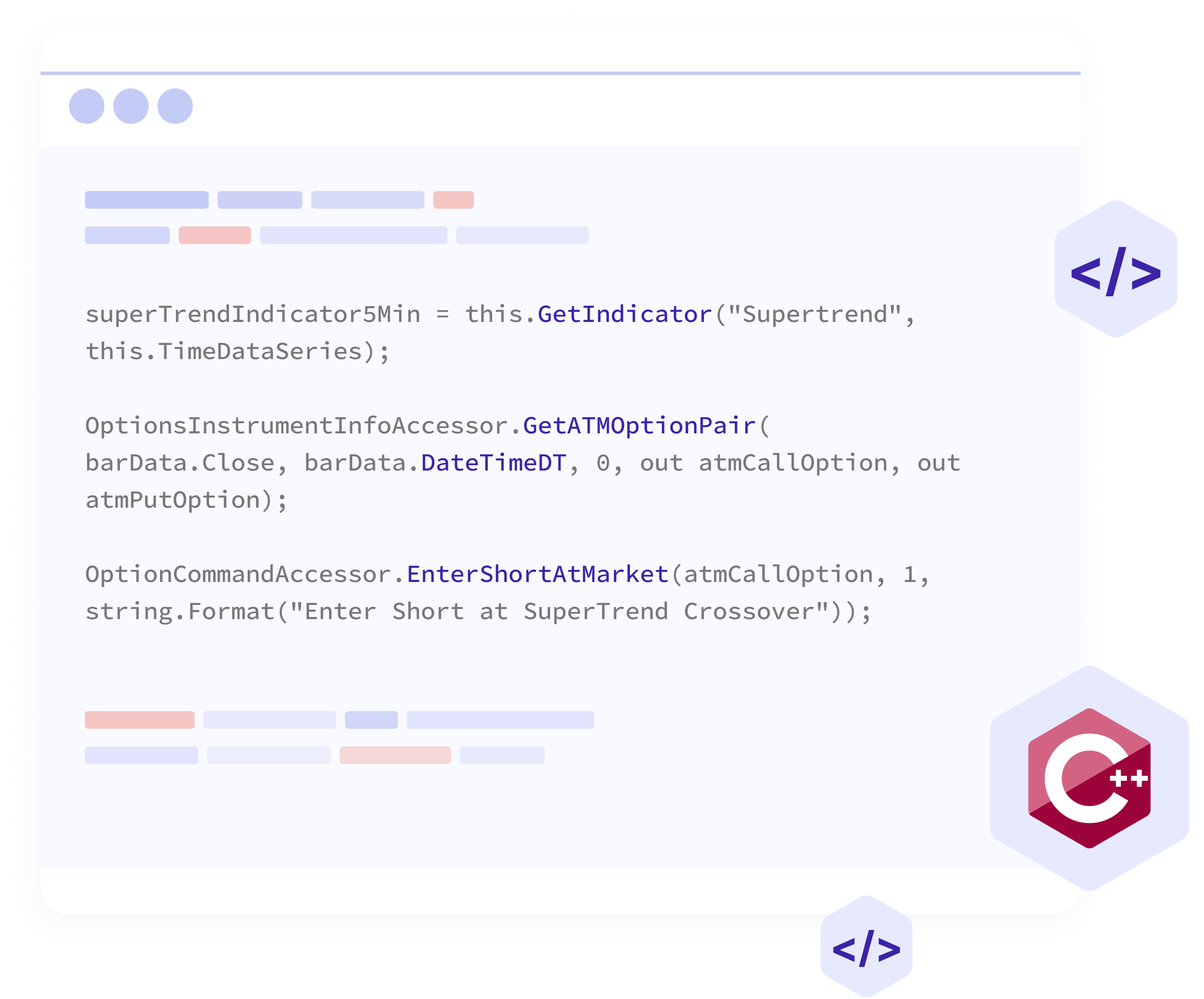

QX.FinLib is a powerful .NET library for rapid development of advanced mechanical trading systems to uncover strategies and pin point opportunities. It simplifies strategy creation, indicator design, and backtesting—including options—with seamless efficiency. Build feature-rich trading applications faster and smarter.

QX.FinLib is a powerful C# library designed for backtesting, analyzing, and optimizing trading strategies. It offers a robust framework to rapidly develop mechanical trading strategies, evaluate performance with precision, and optimize results. Packed with an extensive feature set, QX.FinLib empowers you to build advanced, customized trading system for research and signal generation with ease and efficiency.

We’re here to guide you every step of the way on your mechanical trading system backtesting journey. From tutorials and practical examples to comprehensive resources, we provide everything you need to accelerate your trading system development process and achieve success faster.

Read the Strategy Development Guide

At QuantXpress, we specialize to transform your trading ideas into market-ready strategies. Whether you're looking to validate a new strategy, optimize parameters, or set up a fully automated trading desk, our skilled quantitative researchers, consultant and programmers are ready to assist.

Contact us today to bring your vision to life!

We’re here to guide you every step of the way on your mechanical trading system backtesting journey. From tutorials and practical examples to comprehensive resources, we provide everything you need to accelerate your trading system development process and achieve success faster.

Our comprehensive documentation is packed with robust examples and detailed guides to help you quickly kickstart your trading research, development, and beyond.

Whether you're building strategies, backtesting models, or optimizing systems, our open source GitHub resources are designed to accelerate your workflow and bring your ideas to life.